This vignette1 discusses model checking in fHMM, that means the task of verifying whether the fitted model describes the data well.

Model checking using pseudo-residuals

Since the observations are explained by different distributions (depending on the active state), model checking cannot be done by analyzing standard residuals. Instead, we consider “pseudo-residuals”. To transform all observations on a common scale, we proceed as follows: If has the invertible distribution function , then

is standard normally distributed, where denotes the cumulative distribution function of the standard normal distribution. The observations, , are modeled well if the so-called pseudo-residuals, , are approximately standard normally distributed, which can be visually assessed using quantile-quantile plots or further investigated using statistical tests such as the Jarque-Bera test (Zucchini et al. 2016).

For HHMMs, we first decode the coarse-scale state process using the Viterbi algorithm. Subsequently, we assign each coarse-scale observation its distribution function under the fitted model and perform the transformation described above. Using the Viterbi-decoded coarse-scale states, we then treat the fine-scale observations analogously.

Implementation

In fHMM, pseudo-residuals can be computed via the

compute_residuals() function, provided that the states have

been decoded beforehand.

We revisit the DAX example:

data(dax_model_3t)The following line computes the residuals and saves them into the

model object:

dax_model_3t <- compute_residuals(dax_model_3t)

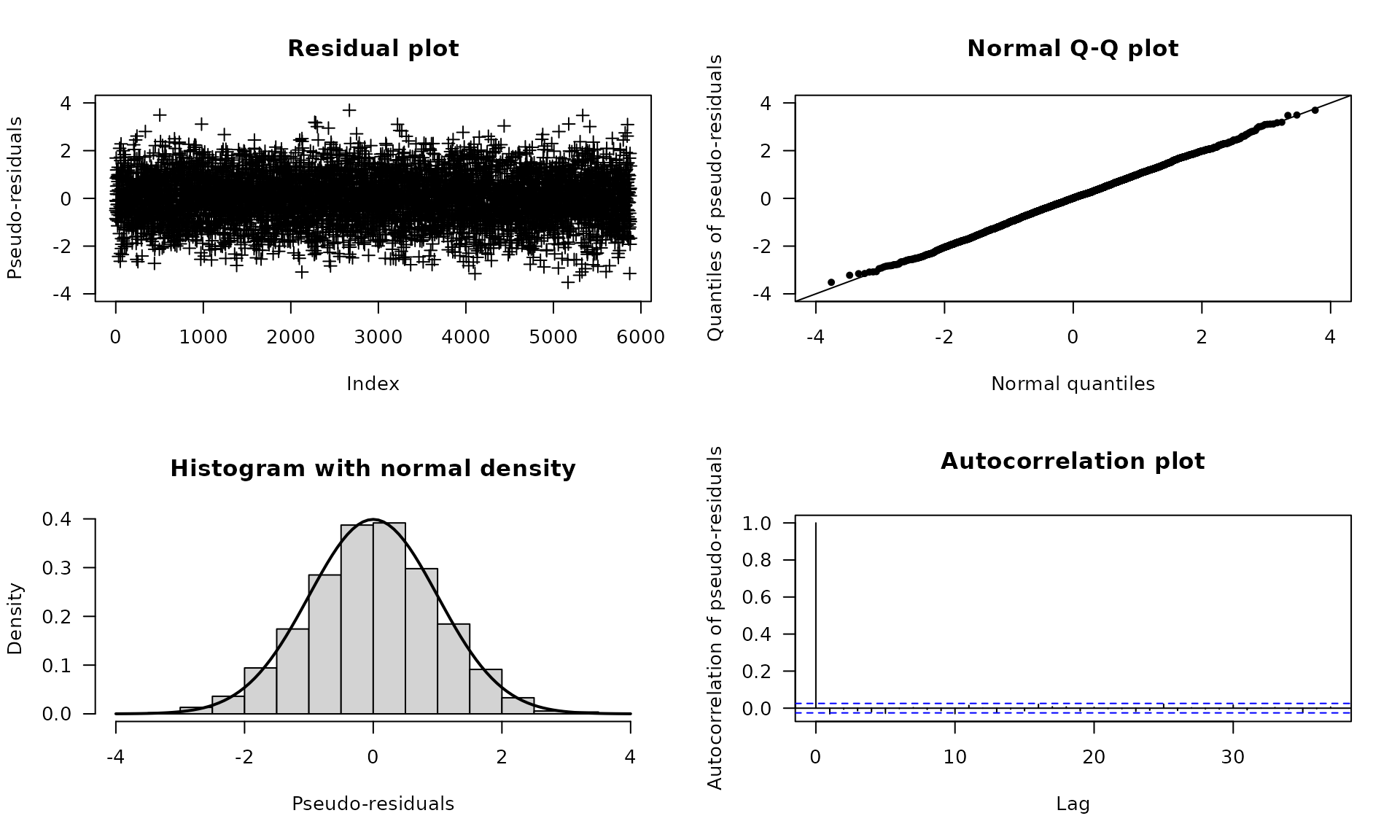

#> Computed residualsThe residuals can be visualized as follows:

plot(dax_model_3t, plot_type = "pr")

For additional normality tests, the residuals can be extracted from

the model object via the residuals() method.

The following lines perform a Jarque–Bera

test as an example (Jarque and Bera 1987):

tseries::jarque.bera.test(residuals(dax_model_3t))

#>

#> Jarque Bera Test

#>

#> data: residuals(dax_model_3t)

#> X-squared = 2.2403, df = 2, p-value = 0.3262